Tether explained

Not the right way.

Stop calling Tether a stablecoin company. That hasn’t been true for a while.

Not since they hoarded 97,000 Bitcoin, backed themselves with $20 billion in gold, and pivoted into secured lending. The token itself is just the plumbing now.

It’s a massive, interest-free deposit base with no insurance and a historically spotty audit trail. Tether is running something entirely different, something much harder to define.

But, Tether found time in May to publish medical language models that run on smartphones.

The models come from QVAC, Tether’s AI research group, and they reportedly outperform larger systems without needing cloud infrastructure. A doctor in a low-connectivity region could theoretically use them on a basic Android device.

If you are wondering what this has to do with a dollar-pegged stablecoin, I like your question. Nobody at Tether seems to be, so i explain this to you.

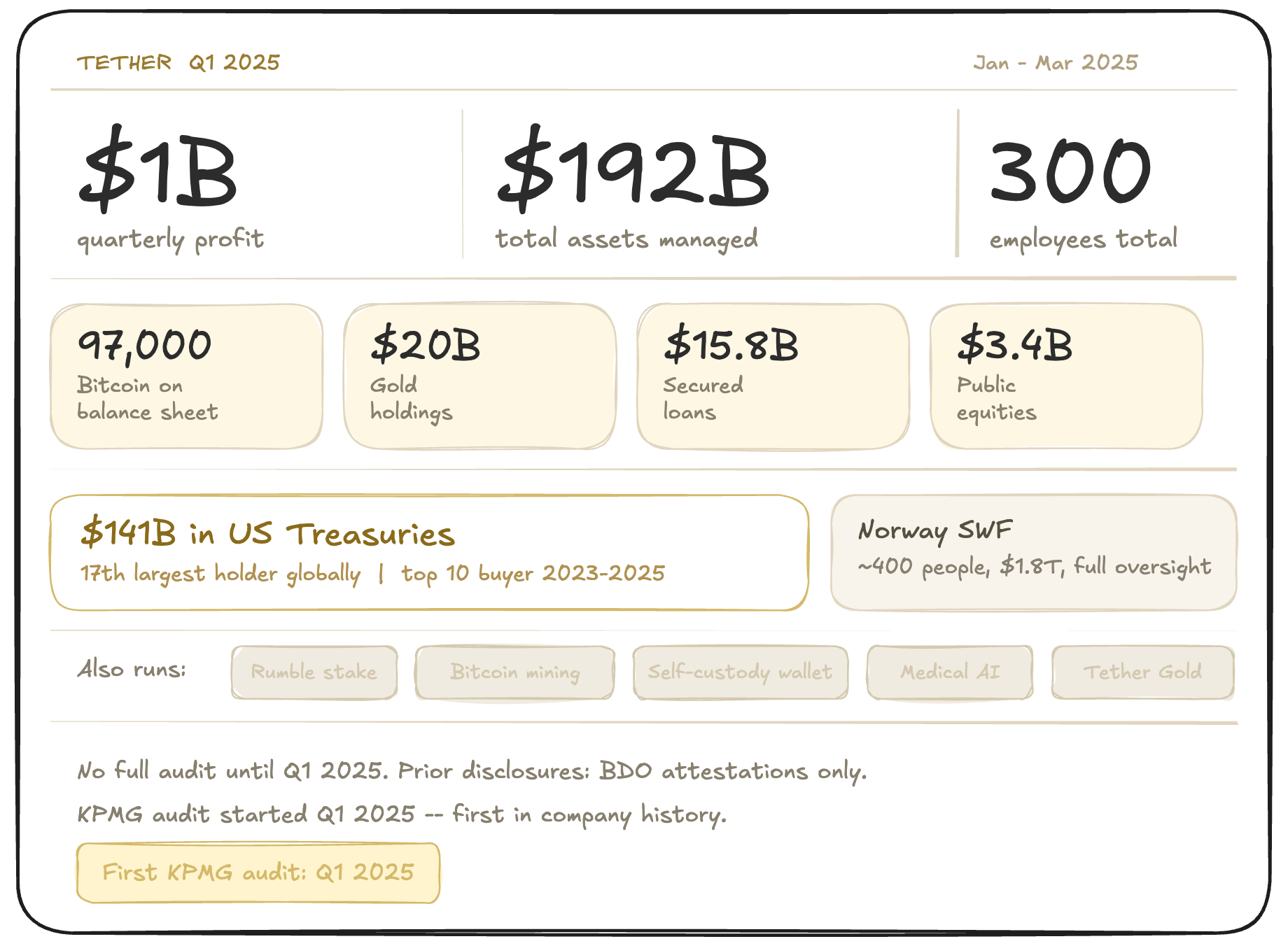

The Q1 numbers: $1 billion in quarterly profit. 97,000 bitcoin on the balance sheet. $20 billion in gold. $15.8 billion in secured loans. $3.4 billion in public equities. Stakes in Rumble. A mining operation. A wallet. Medical AI. Three hundred employees managing $192 billion in assets.

Norway’s sovereign wealth fund has roughly 400 employees managing $1.8 trillion. The regulatory apparatus around it runs hundreds of pages. Tether has 300 people, $192 billion, and until Q1 of this year, no auditor.

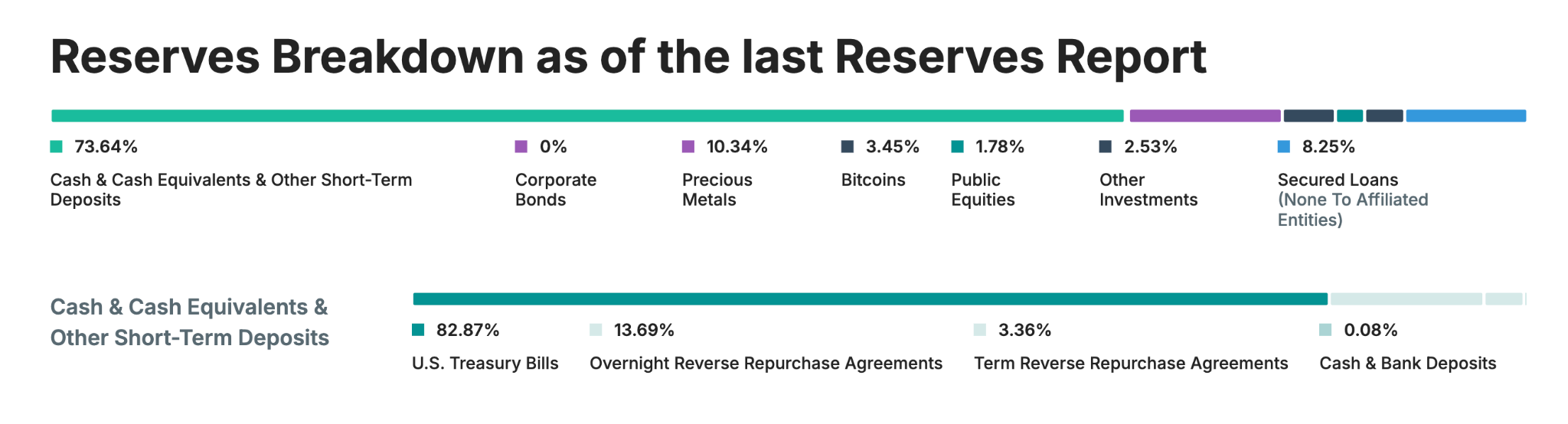

Strip the structure down. Tether issues USDT. People deposit $183 billion worth of dollars to hold it. Tether takes those deposits and invests them in US Treasuries, gold, bitcoin, equities, secured loans, and AI companies.

The yield on those investments is the profit. USDT is the liability and everything else is the asset.

That is a bank. One that takes deposits, pays no interest, invests aggressively, and keeps the spread. Just a quarterly attestation from BDO confirming the reserves exist on a specific date.

KPMG started a full audit in Q1. First one ever. An attestation and an audit are different things. Attestations confirm specific numbers at a point in time, audits examine the systems and accounting practices that produced those numbers. Attestations tell you what Tether says it holds. An audit examines whether Tether accounts for those holdings are trustworthy.

Why now? Tether would say it is growing up. My reading is that four congressional investigations and an incoming federal stablecoin framework made an audit a better option than the alternative.

Tether holds $141 billion in US Treasuries. Seventeenth largest holder globally. One of the top ten buyers over the past two years.

The US government currently runs a deficit that requires it to sell a lot of Treasuries. It needs buyers. Tether is a very large buyer. This creates an arrangement where the US government is simultaneously one of Tether’s most important business relationships and the source of its biggest regulatory threat.

The GENIUS Act, signed into law in July 2025, established the first federal framework for stablecoin issuers. USDT’s reserve composition, its El Salvador domicile, and its redemption structure were not built for OCC supervision. Rather than retrofitting USDT, Tether launched a separate product.

USAT went live January 27, 2026. Issued by Anchorage Digital Bank, which holds a federal OCC charter. Bo Hines, previously executive director of the White House crypto advisory council, runs it. Available on Kraken, Crypto.com, Bybit, and OKX, on Ethereum and Tron, with more chains coming.

The split makes sense on its face. USDT keeps serving its existing markets, concentrated in emerging economies where dollar access is genuinely difficult.

USAT serves US institutions and regulated DeFi protocols that need a compliant domestic dollar token.

Who custodies USAT’s reserves? Cantor Fitzgerald. Same firm that custodies 99 percent of USDT’s $141 billion in Treasuries. Same firm holding a 5 percent equity stake in Tether. Same firm whose former CEO is now US Secretary of Commerce.

Howard Lutnick ran Cantor Fitzgerald for decades. Under his leadership, Cantor became Tether’s primary Treasury custodian and at some point acquired a 5 percent stake in Tether itself. In February 2025, Lutnick was confirmed as Secretary of Commerce. His family trust retained its Cantor interests.

On April 30, Senators Warren and Wyden opened their fourth investigation into this arrangement. The same week, GENIUS Act implementing rules were heading through committee.

Lutnick’s defenders note he has recused himself from specific Cantor-related decisions, and that the Treasury custody relationship predates his government role. Fine. A company under four active congressional investigations has its financial plumbing managed by a firm whose founder sits in the cabinet. No one needs to do anything wrong for that to be a problem.

Now add the $344 million.

On April 23, OFAC designated two Tron wallet addresses as property of Iran’s Islamic Revolutionary Guard Corps. Tether froze $344 million in USDT across those addresses the same day, in coordination with OFAC and US law enforcement. One wallet held approximately $213 million, the other approximately $131 million. TRM Labs traced them back to roughly 1,000 transactions dating to March 2021, with most funds going dormant after late 2023 -- the pattern looked like reserve storage rather than active operational use.

Tether called this law enforcement cooperation.

Last week, a group of terrorism judgment creditors filed in the Southern District of New York asking a federal judge to compel Tether to transfer the frozen funds to them.

The plaintiffs hold billions in unpaid US court judgments tied to Iranian-backed attacks. Their argument is that OFAC already designated the wallets as Iranian property, Tether has already demonstrated it can zero out balances and reissue USDT to a new address, so redirect these funds toward people with legal claims against Iran.

The case is undecided. What it surfaces is worth sitting with. Tether froze $344 million in under 24 hours. Those funds now sit immobilized on Tether’s ledger. If Tether wins this case, a stablecoin issuer can freeze assets but owes nothing to judgment creditors. If the plaintiffs win, stablecoin issuers function as quasi-custodians subject to court-ordered transfers.

Either way, you are describing an institution that can freeze nine figures of assets overnight and then exercise discretion over what happens to them. That is not a compliance function. Most regulated financial institutions do not hold that power unilaterally.

In December 2025, Tether took a Bitcoin treasury company called Twenty One Capital public on the NYSE under ticker XXI. 43,500 bitcoin at launch, third-largest public corporate holder. Jack Mallers as CEO. SoftBank as minority owner. The SPAC that brought it public belonged to Cantor Fitzgerald.

Of course it did.

On April 29, Tether proposed merging XXI with Strike and Elektron Energy, a mining operator running roughly 5 percent of the Bitcoin network’s total computing power. Treasury, mining, payments, lending. One NYSE ticker. Tether Gold hit new highs as gold surged. The Tether Wallet launched April 14. And QVAC shipped the medical AI.

Does Tether have the reserves? Is it audited? Can it be trusted? Reasonable questions in 2019. I don’t have answers.

Tether issues a currency held by hundreds of millions of people. It moves Treasury markets. It freezes assets on federal request. It runs a $20 billion gold position and has 300 employees and no shareholders.

We have frameworks for banks, asset managers, exchanges, and now stablecoin issuers. None were built for something that is all of these simultaneously, domiciled offshore, generating $1 billion per quarter, and answerable to nobody in particular.

Congress is investigating. Four times now. The rules are still being written.

Somewhere in all of this, QVAC released the medical AI.